UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A

(Rule 14a-101)

INFORMATION REQUIRED IN PROXY STATEMENT

SCHEDULE 14A INFORMATION

Proxy Statement Pursuant to Section 14(a) of The Securities Exchange Act of 1934

(Amendment No. )

Filed by the Registrant ☐

Filed by a Party other than the Registrant ☒

Check the appropriate box:

| ☐ | Preliminary Proxy Statement |

| ☐ | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) |

| ☐ | Definitive Proxy Statement |

| ☒ | Definitive Additional Materials |

| ☐ | Soliciting Material Under Rule 14a-12 |

| Synalloy Corporation |

(Name of Registrant as Specified in Its Charter) |

Privet Fund LP Privet Fund Management LLC Ryan Levenson UPG Enterprises LLC Paul Douglass Christopher Hutter Andee Harris Aldo Mazzaferro Benjamin Rosenzweig John P. Schauerman |

(Name of Persons(s) Filing Proxy Statement, if Other Than the Registrant) |

Payment of Filing Fee (Check the appropriate box):

| ☒ | No fee required. |

| ☐ | Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. |

| (1) | Title of each class of securities to which transaction applies: |

| (2) | Aggregate number of securities to which transaction applies: |

| (3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined): |

| (4) | Proposed maximum aggregate value of transaction: |

| (5) | Total fee paid: |

| ☐ | Fee paid previously with preliminary materials: |

☐ Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the form or schedule and the date of its filing.

| (1) | Amount previously paid: |

| (2) | Form, Schedule or Registration Statement No.: |

| (3) | Filing Party: |

| (4) | Date Filed: |

Privet Fund LP and UPG Enterprises LLC, together with the other participants named herein (collectively, the “Stockholder Group”), has made a definitive filing with the Securities and Exchange Commission of a proxy statement and accompanying WHITE proxy card to be used to solicit votes for the election of the Stockholder Group’s slate of highly qualified director nominees to the Board of Directors of Synalloy Corporation, a Delaware corporation (the “Company”), at the Company’s upcoming 2020 annual meeting of stockholders, or any other meeting of stockholders held in lieu thereof, and any adjournments, postponements, reschedulings or continuations thereof.

Item 1: On April 24, 2020, The Deal published the following article:

Activist Spotlight: CEOs Under Attack as M&A Fades

Last month, Punch Card Capital LP, a Florida-based $360 million investment fund, launched a campaign urging the CEO of motor-home manufacturer Winnebago Industries Inc. (WGO) to forgo compensation after the company announced furloughs, layoffs and reduced employee pay.

We read that affected employees... will be left with two weeks of pay, but we did not see any mention of reductions taken at the executive level at corporate headquarters in Eden Prairie, Punch Card founder Norbert Lou noted in a letter.

In response, on April 3, the company announced plans to cut CEO Michael Happe’s salary by 25% and eliminate incentive payments for the remainder of fiscal 2020. Winnebago’s board also saw their cash compensation lowered by 25% for the year.

It’s unclear if the move was enough for Punch Card. Either way, the insurgency represents a shift in approach to activism that has emerged with the coronavirus pandemic. Instead of focusing on M&A and stock buybacks, which, until recently, were among the most popular strategies, insurgents are focusing on CEO pay, performance and operational issues.

But out of concern, perhaps, that M&A and buybacks could generate a public backlash at a time of economic distress, activist funds are seeking to remove CEOs they contend are overpaid and not qualified to oversee companies struggling to deal with the effects the pandemic.

Activists focus on the opportunities at hand, said Andrew Freedman, partner at Olshan Frome Wolosky LLP in New York. If we’re in a period where certain alternatives like transactions and buybacks aren’t on the table that doesn’t mean that there aren’t significant other opportunities to improve performance and create value. Activists want to ensure that boards and management teams are appropriately evaluating those opportunities.

Statistics released April 16 by investment bank Lazard provides detailed evidence of the shifting strategies. The bank noted that only five of 16 campaigns initiated in March at companies with greater than $500 million market capitalizations had an M&A thesis. In the first quarter of 2019 and 2018, 27 and 23 campaigns came with M&A strategies, respectively. The Lazard report acknowledged the change, noting that activists will face near-term challenges in urging consolidation or divestitures as M&A activity [sinks] to multi-year lows.

Expect even fewer insurgency campaigns to focus on driving dividends or buybacks as corporations focus on preserving cash. At the same time, some government stimulus packages include provisions prohibiting recipients from returning capital to shareholders, essentially taking the share-price-improving lever of buybacks away from activists. Only one campaign in the first quarter of 2020 had a capital return thesis, Lazard noted.

Lawrence Elbaum, partner and co-head of Vinson & Elkins shareholder activism practice in New York, argued that activists have refrained, for the most part, from M&A or capital-allocation campaigns because the markets haven’t stabilized yet. Activists generally won t push for dividends, divestitures or auctions because they don t know the extent of the Covid-19-driven sell-off, he added. However, insurgencies targeting CEOs and perceived operational failures continue.

There are companies that, going into the crisis, activists alleged were mismanaged and undervalued, he said. With the market dislocation and major parts of the economy shut down, it is not surprising that these same activists will argue that boards and management teams that they insisted were ill-equipped to lead during a boom should not be leading during a crisis.

In fact, a large component of Covid-19-period activist campaigns go far further than requesting pay package reductions. Investors in many cases are seeking to take control of boards and remove C-Suite executives. Also, activists are publicly warning companies against selling businesses during the crisis.

Consider Privet Fund Management LLC campaign to take control of the board of metal sand specialty chemical company Synalloy Corp. (SYNL). The fund, which made an unsuccessful bid to buy the company last year, doesn’t want to acquire it now or see it sold. Instead, founder Ben Rosenzweig is hoping to oust management and drive an operational turnaround.

If you can t drive results and effectively manage a company during the past decade, that might ultimately go down as one of the greatest decades of economic expansion that most people have lived through, why should shareholders want the current team to lead the company through a pandemic situation? Rosenzweig said.

At Merit Medical Systems Inc. (MMSI), Starboard Value LLC s Jeff Smith may be pushing to oust the medical device manufacturer’s founder and CEO Fred Lampropoulos.

Starboard has another contest underway at GCP Applied Technologies Inc. (GCP), where it appears to want changes in the chemical and construction materials company s C-Suite. In an April 2 letter, Starboard said it recognizes the Covid-19 crisis has created a difficult environment for many companies but that GCP needs “strong leadership and oversight” during and after the crisis, comments suggesting that the fund believes a CEO change is necessary.

Another activist, Ex-Third Point LLC analyst Michael Gorzynski, wants to take control of the board of miniconglomerate HC2 Inc. (HCHC) so it can eject CEO Philip Falcone. In the campaign, Gorzynski argues that Falcone and the company’s management team are overcompensated while its board puts the business on a path to bankruptcy. The fund s overall campaign seeks to slash expenses, debt and what it insists are problematic related-party payments.

Other campaigns focus on CEO pay packages. Voce Capital s J. Daniel Plants is urging investors to vote against three directors up for election at OnDeck Capital Inc. (ONDK) at its meeting May 7 over his concerns around misaligned executive compensation, governance failures and a lack of strategic focus. Plants notes that he pleaded with the small business lending company last month to reduce expenses, but he hasn’t seen any action taken yet.

Then there’s labor-backed CtW Investment Group s new campaign at Uber Technologies Inc. (UBER), where the fund argues that CEO Dara Khosrowshahi s pay is overly generous, that the coronavirus has exposed shortcomings in the ride-sharing company s business model, and that investors should vote against the election of audit committee chair John Thain over worries about his previous oversight of Merrill Lynch and CIT Group Inc. (CIT).

Finally, Impala Asset Management LLC on March 30 settled its dispute with Harley-Davidson Inc. in a deal that allows the fund to weigh in on a new director candidate. The fund, which has complained about executive compensation packages, also claimed to have a role in Harley’s February decision to terminate CEO Matt Levatich.

Meanwhile, however, many insurgents will halt their plans until they can gain a clearer idea of the extent of the crisis, though this month’s quarterly financial results may help.

A lot of activists probably don t want to wage a specific capital allocation campaign in the middle of the pandemic, particularly as the most recent quarter s earnings reveal themselves and we start to see a picture revealing the extent of the economic damage, Elbaum said.

(emphasis added)

Source: The Deal. The Deal is not a party to and has not endorsed our proxy solicitation and has not consented to the use of this podcast interview in our proxy solicitation.

Ronald Orol for The Deal.

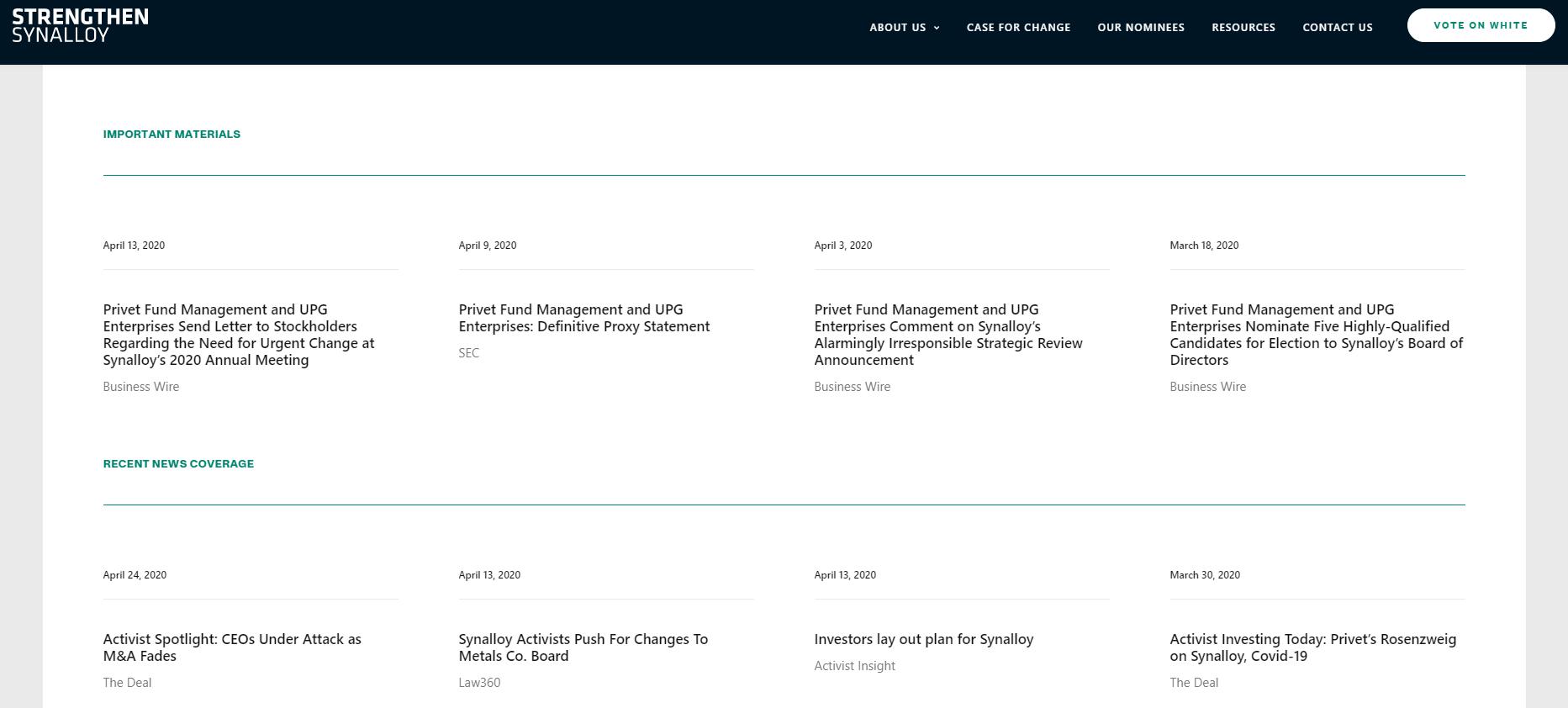

Item 2: On April 24, 2020, the following materials were posted by the Stockholder Group to www.StrengthenSynalloy.com:

Item 3: The Stockholder Group has issued the following digital advertisements: